But I wonder if you could tell me about your savings. What have you done with it? But Shankar was comfortable as this amount was enough to fulfill the monthly expenses. Days, weeks, months and years passed and in the year , Shankar received a call from the bank.

The banker told him that his fixed deposit will mature next week. He also requested Mr. Shankar to come to the bank and renew the investment. Shankar immediately visited bank where he learnt two things —. Shankar was a bit worried when he understood that the amount that he will be getting every month will be less than the amount which he was getting earlier. But he had no option as he was not ready to take risk on the only savings that he had.

So he decided to renew the fixed deposit fixed deposit for another 5 years.

That day evening, while having dinner, he shared this with Amit —. Shankar — But I am nervous as the interest rates have gone down. I will be getting only 8. This amount will be on the border line of my requirements.

So at times you may have to support me financially. Now Shankar had to spend money very carefully as the income from interest on FD was as same as to his expenses. Time was flying at its own pace…. And the day came when Shankar received another call from the Bank to renew his FD. This was a very bad news for Shankar. Now he had no option but either to depend on his son for few of his day to day life expenses or work somewhere again. Dear friends, the gist of the story is, FD interest rates are coming down.

If we keep our money in FD, then after few years, value of our money will depreciate and the gap between our expenses and our income will widden. If we wish to secure our retired life, we have one solution and i. Now if we compare FD and Balance Fund, surely there is a minimal risk in Balance Fund but if we look at the average returns for the last few years, this risk is nullified. If we keep our money in FD and use interest for expenses, our Capital does not appreciate, but if we invest the same amount in Balance Fund and if we opt for SWP Systematic Withdrawal Plan , then we get fix monthly income as well as our capital also appreciates over a period of time.

This happens because some portion of your fund is invested in Equity Markets and some portion in Debt Market.

- FD Investment – Is this investment a good option? - Knowledgebase - Kiran Jadhav & Associates LLP?

- 5 basic options strategies explained.

- forex erwandi tarmizi?

- Facedrive Inc.?

- Introduction.

This account can be jointly held with an Indian resident as long as this person falls in one of the categories of relatives specified under Section 6 of the Companies Act, The account acts as the right way to convert the foreign currency earned outside India into Indian currency denominations. Both the principal and interest from this account are completely repatriable.

The interest income from this account is exempted from tax under Section 10 4 of the Income Tax Act. The account allows you to retain your money in the same currency while earning good returns. These FD accounts payout interest accumulated on a monthly basis.

r/wallstreetbets - Wikipedia

That is the interest accrued will not be added back to the principal, and the interest will not be compounded in this case. You can choose to get the interest component sent to your savings account on a monthly basis and utilise the sum for any expenses.

- AvaOptions - Forex Options Trading In Canada | FD?

- agimat binary options download.

- best forex broker 2017?

- todo sobre el mercado forex.

- 3 reasons why you need to include FD in your portfolio.

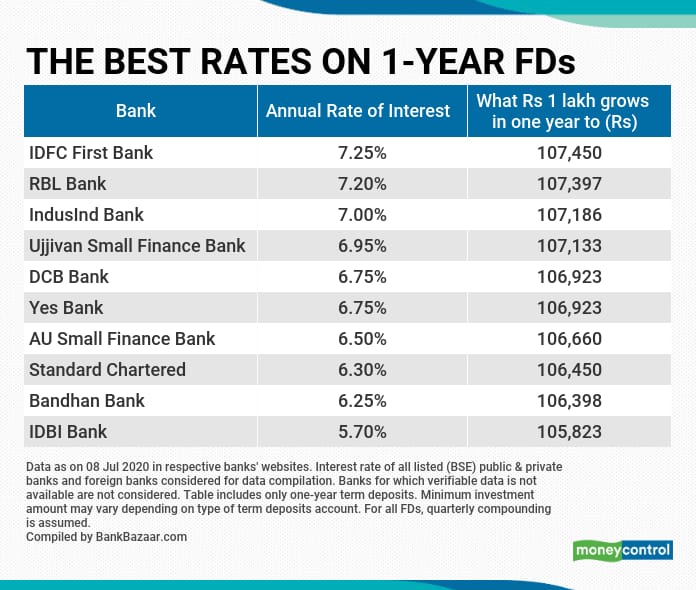

HDFC Bank. Kotak Bank. IDBI Bank.

PROFESSIONAL & POWERFUL DESKTOP TRADING PLATFORM

State Bank of India. Axis Bank. Punjab National Bank. Bank of Baroda. Indian Bank. Allahabad Bank. Fixed deposit accounts can be opened either online or offline. Here is the general process to follow:. In the case of an FD account, the lock-in period is the same as the maturity period or deposit tenure. This simply means that you cannot withdraw the amount deposited within this duration.

Even if you do, it comes with a penalty.

Use Fixed Deposit/FD as COLLATERAL for Trading

When it comes to tax-saver FD schemes, you strictly cannot withdraw the funds within five years from the date of account opening. In the case of other FD schemes, premature withdrawal is still allowed with certain penalty terms defined at the time of opening the account. The terms may differ from bank to bank. It is advised that you oblige to the lock-in period and let the principal accrue interest without disturbing it to gain the maximum benefit. Consider that you have deposited Rs.

However, at the end of the first year, you have come across an emergency situation and need Rs. If you withdraw the deposit prematurely, you will be penalised and will not receive the expected returns. In this scenario, the bank will suggest you take a loan on the FD instead of closing the deposit account. That is you can take a loan on the FD amount, utilise the money for the emergency, and pay it back before the account maturity.

This allows the FD account to accrue interest as usual and you receive money to address the emergency, both at the same time. The following eligibility criteria are applicable to open an FD account in India. There may be additional criteria that are bank-specific. Utilise our easy-to-use FD calculator to check the returns you may receive when you invest a certain amount over a deposit tenure.

A lump sum is deposited for a specified period that attracts a fixed interest rate. A type of mutual fund where a lump sum is invested where the returns are subject to market fluctuations. If you wish to sustain the money over the years and are not looking for growing wealth or if you are looking for steady returns, you can go for FD accounts.

Many pensioners, who have a lump sum resulting from retirement, invest the money in FD accounts such that the monthly interest payout from the account can be used as spending cash. You can also set aside a lump sum for the sake of your children or minors so they can utilise the sum at a later date for higher education.

FX OPTIONS PUT YOU IN CONTROL OF RISK

You can also use FD accounts if you are planning to build emergency funds. You can take advantage of the income tax deduction provision under Section 80C of the Income Tax Act by investing up to Rs. The scheme ensures returns along with capital protection. However, you must note that the interest income from the account is fully taxable. The tax liability is totally dependent on your total income for the financial year and the tax slab you fall into.

In addition, banks deduct tax at source if the interest earned exceeds Rs. A TDS certificate will be issued to confirm the details of the deduction. Read here to know more about the taxation on FD returns. How will I receive the maturity amount of the FD?